Indiana-based banks see stock-price rebound on horizon

Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

Indiana-based banks, and publicly traded banks nationwide, have seen their stock prices take a beating this year—but bank executives and analysts are optimistic that the slump is nearing an end.

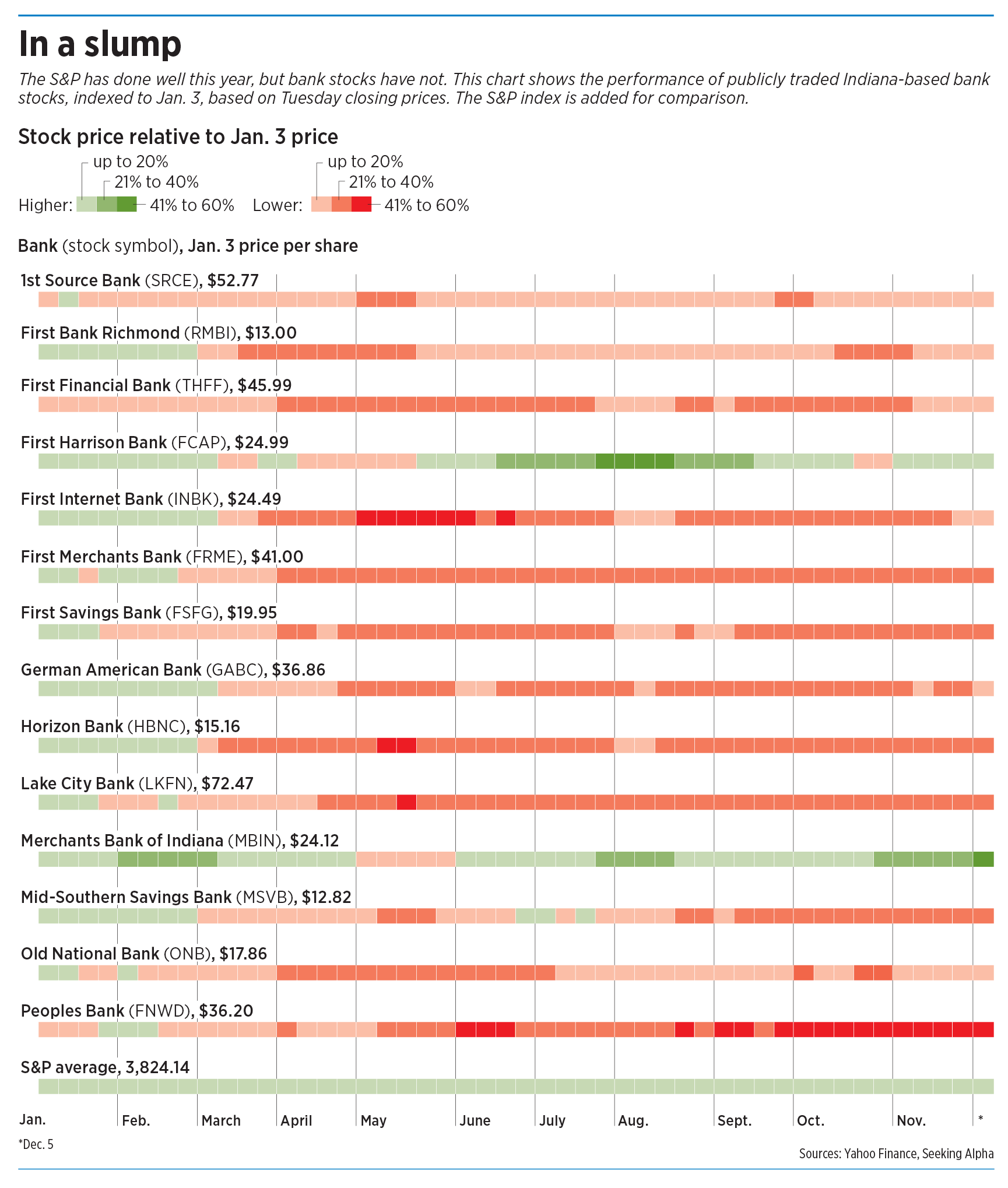

Unlike bank stocks, the broader S&P 500 has shown consistent growth. As of Tuesday, the S&P was 4,567.18, up 19.4% from the beginning of the year.

Among Indiana’s 14 publicly traded banks, however, most have seen a significant drop in stock prices at some point, in some cases falling more than 50% from their Jan. 3 prices, the first trading day of the year. As of Tuesday, six of the Indiana banks were still trading at least 20% below where they traded in January.

“It hasn’t been this bad since coming right out of the [2008-2009] financial crisis,” said Nathan Stovall, a banking analyst with S&P Global Market Intelligence. “The banks are down a lot.”

It’s not that Indiana-based bank stocks are especially poor performers, the bankers and analysts say, noting bank stock prices are down industrywide, even as banks have generally remained profitable. Rather, it’s that the uncertainty fueled by recent interest-rate hikes is posing a challenge to the industry.

As recently as March 2022, the effective federal funds rate—the volume-weighted median interest rate banks pay to borrow from other banks—was 0.08%. Following a rapid series of rate hikes by the Federal Reserve, that rate increased to 5.33% by July of this year, and it remains at that level.

The rapid rise in interest rates affects banks and their stock prices in a few ways.

For one thing, the uncertainty it introduces can spook investors.

“You know, 70% of [banks’] revenue comes from interest rates. And so, when interest rates are volatile, moving around, that could put uncertainty around the future value of bank stocks,” said Jim Ryan, CEO of Evansville-based Old National Bank, Indiana’s largest home-grown bank in terms of assets.

Old National’s stock, which closed at $17.86 on the first trading day of 2023, closed as low as $12.10 this year—on May 11—a 32% drop from its Jan. 3 price. The stock has partially rebounded since, closing at $15.88 on Tuesday.

Right now, Ryan said, the uncertainty in the financial sector has driven away many generalists who invest in multiple sectors. “The people that don’t have to invest in banks today aren’t investing in banks.”

Mark Hardwick, CEO of Muncie-based First Merchants Bank, pointed to another dynamic.

Larger banks tend to have more of those generalist investors, he said. Smaller banks tend to attract investors who specialize in the financial sector and understand more about banking. They tend to be less skittish in times of uncertainty.

“Those of us that have a little more mutual fund exposure haven’t performed quite as well as those that have more specific bank-stock-specialty investors,” Hardwick said.

First Merchants stock, which had a Jan. 3 closing price of $41 per share, also hit its low point on May 11, closing at $24.89—a 39% drop from that Jan. 3 price. The stock closed at $32.59 on Tuesday.

Other challenges

Higher interest rates can also hurt banks if they hold a lot of fixed-rate loans or investments. This is because the amount they can earn from these fixed-rate assets stays the same as interest rates climb. Meanwhile, depositors expect to see higher interest rates on savings accounts and CDs.

About 70% of First Merchants’ loans are variable-rate loans, Hardwick said. Most of the bank’s commercial loans have interest rates that can be adjusted daily, he said, so the bank has been able to raise borrowers’ interest rates as the federal funds rate has gone up. About 75% of the bank’s $12.3 billion loan portfolio is in commercial loans.

Another point of uncertainty around rising interest rates: Will they slow the economy to the point that loan-delinquency rates rise?

So far, Old National’s Ryan said, that hasn’t happened. “The industry’s been very resilient, and losses have been very mild—but the potential exists because of what the Fed is doing in terms of raising interest rates.”

Another cause for uncertainty comes from a handful of high-profile bank failures last spring: California-based Silicon Valley Bank and New York-based Signature Bank in March, and California-based First Republic Bank in May.

A Federal Reserve report issued April 28 specifically cited Silicon Valley Bank’s failure to manage interest-rate risk as a factor that led to its collapse.

The bank, which focused on tech-sector clients, occupied a unique niche. But its failure cast a cloud over the banking industry overall, said Nate Race, a Chicago-based senior research equity analyst at investment bank Piper Sandler Cos. “It definitely spooked investors and bank management teams.”

Stovall, the S&P analyst, agreed. “The fear factor of what went down in March sent money out of [bank stocks], and it hasn’t come back in.”

Among the banking industry’s outliers is Carmel-based Merchants Bank of Indiana, whose stock closed Tuesday at $35.25—its highest closing price since the bank went public in 2017. That price is up 46% from its Jan. 3 closing price of $24.12.

“We have a very different business model,” said Merchants Bank President Michael Dunlap. “We’re in some businesses that traditional banks don’t enter into.”

Merchants Bank’s focus is on loans to developers of affordable multifamily residential developments and health care properties. Its loans are underwritten to the standards of government agencies such as the Federal Housing Administration, Fannie Mae and Freddie Mac, making them less risky.

The bank also originates loans with the intent to sell them off rather than hold them, which offers protection from interest-rate risk.

Hopeful signs

But for the banks whose share prices have floundered this year in Indiana and beyond, analysts and bankers see signs that things are picking up.

In particular, Race said, November was a good month for Indiana bank stocks. For the year, through November, the median price decline for 11 Indiana bank stocks was 23%. But that same group saw a 12% median stock-price increase during November alone.

Indiana’s strongest gainer last month was Fishers-based First Internet Bank, which saw its stock price rise 34%. The only bank in the group to see its stock price decline was Clarksville-based First Savings Bank with a 1% drop.

Optimism is also growing that the days of frequent rate hikes are over.

The Federal Reserve held interest rates steady at its September and November meetings, and a recent story from The Wall Street Journal carried the headline: “Fed’s Interest Rate Hikes Are Probably Over, But Officials Are Reluctant to Say So.”

“We’re finally reaching that point that there is some clarity that the Fed’s probably done,” Hardwick said, adding that there’s even been speculation that rates might go back down, easing the pressures banks have been facing.

Stovall said banks posted positive earnings reports in the second and third quarters, but he predicted it will take another two or three quarters of strong earnings before many investors feel comfortable returning to the banking sector.

Ryan, who described himself as an optimist by nature, said he’s buoyed by the fact that banks have generally performed well this year even if their stock prices have slumped.

“Most Indiana banks are relatively healthy, and the industry’s healthy and will continue to be strong,” he said.